CIP – Carriage and Insurance paid to

Definition of CIP (Carriage and Insurance paid to)

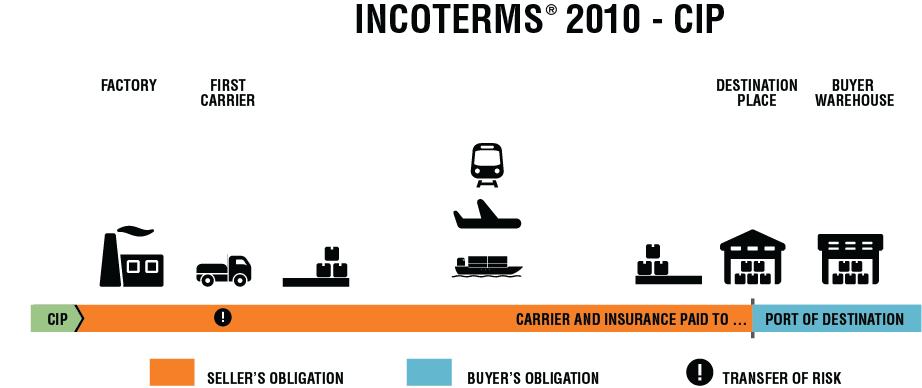

CIP (or Carriage and Insurance Paid To) is an Incoterm where the seller is responsible for the delivery of goods to an agreed destination in the buyers country, and must pay for the cost of this carriage. The sellers risk however, ends once they have placed the goods on the ship, at the origin destination. The buyer can pay for additional insurance during carriage of the goods. The risk is passed when the goods are received by the first carrier.

Carriage and Insurance Paid to is eligible for any form of transportion.

CIP Incoterm Buyer & Seller Obligations

Under the Incoterms 2020 rules, CIP means the seller is responsible for delivering goods to the first carrier or another person stipulated by the seller at a named place of shipment, at which point risk transfers to the buyer. The seller is responsible for the transportation costs and insurance associated with delivering goods at least to the named place of destination.

CIP is one of only two Incoterms 2020 rules that identify which of the parties must purchase insurance (the other being CIF—Cost, Insurance and Freight).

With the release of the Incoterms 2020 rules, the amount of insurance required under CIP has increased to at least 110% of the value of the goods as detailed in Clause A of the Institute Cargo Clauses rather than the lower level provided under Clause C, which is what was required for CIP in the 2010 rules and still is required for CIF. This is because CIP is most commonly used for manufactured goods with higher value than the commodity goods more typically shipped under CIF.

Since this is a standard export transaction, the seller or its agent is responsible for submitting the Electronic Export Information (EEI) through AESDirect on the ACE portal.

Seller’s Obligations

- Carrying out all the duties under the terms of delivery specified in the contract.

- Handing over the goods to the carrier on the agreed date stated in the contract.

- Contracting or organizing the carriage of the goods from the agreed point of delivery to the named place of destination.

- Operating according to all transport-related security requirements for transport to the destination.

- Packaging and marking the goods.

- Assisting the buyer in obtaining any documents necessary for transit and import clearance formalities.

Buyer’s Obligations

- Taking delivery of the goods.

- Carrying out and paying for import clearance.

- Obtaining documents necessary for import and transit.

- Assisting the seller, at his request, risk, and cost, in obtaining any documents necessary for the export formalities.

- Informing the seller about the place and date of delivery.

CIP Transportation options

The ICC has divided the 11 Incoterms into those that can be used for any mode of transportation and those that should only be used for transport by “sea and inland waterway.” Under Incoterms 2020, CIP can be used for any mode of transportation. This also applies to the use of more than one mode of transport.

CIP Delivery of Goods

In the CIP Incoterms rule, delivery of the goods is the moment of handing over the goods to the carrier. If there are several carriers, the seller is liable for the goods only until they are handed over to the first carrier. The risk related to the damage or loss of the goods transfers from the seller to the buyer at the time of placing the goods, e.g. on a ship or a train.

It is noteworthy that after the delivery of the goods to the carrier, the seller does not guarantee that the goods will arrive at the destination in good condition, in a specified quantity or at all. Nevertheless, the seller must conclude a contract for the carriage of goods from the place of delivery to the agreed destination.

Advantages and Disadvantages of CIP – Cost and insurance paid to

CIP first appeared in Incoterms® 1980 as standing for Freight Carriage and Insurance Paid To, but was shortened in the 1990 rules.

The only difference between CPT and CIP is that the CIP seller must contract for insurance against the buyer’s risk. The level of cover has been changed in Incoterms® 2020 to be the maximum of Institute Cargo Clauses (A), (Air) or similar, for 110% of the CIP value, or similar — what is sometimes referred to as an “all risks” cover.

CIP (Cost and insurance paid to) and Letters of Credit

As with the other “C” rules, a good choice for transactions involving letters of credit.

If payment is by LC the seller should be careful about the wording as some issuing banks have either not progressed beyond the 1970s or simply make up their own clauses. The LC should ideally call for “One original of insurance policy or certificate for 110 percent of full CIP value of the goods shipped covering Institute Cargo Clauses (A) or (Air), Institute War Clauses (Cargo) or (Air Cargo) and Institute Strikes Clauses (Cargo) or (Air Cargo). Banks love to add nonsense clauses like “claims payable in X country” which in the 21st century is outdated thinking as insurers no longer hand over cheques, they pay electronically usually from wherever their head office is. Any wording such as “in the currency of the draft” is equally nonsense as the insurer has no idea of what the draft is, and the LC rules require the insurance to be in the LC currency anyway so it need not be said in the LC itself. Another favourite of bankers who have never read the Institute Cargo Clauses (A) wording is to include in the LC a requirement for the insurance document to state “from seller’s warehouse to buyer’s warehouse” or words to that effect. ICC(A) article 8.1 is already clear as to the duration of coverage and such words on the document either would not make a scrap of difference or could possibly lead to a problem. Nothing more is needed than the above words, anything more is usually redundant and/or dangerous and could lead to a discrepancy.

Differences between CIP 2020 and CFR

This rule too dates back to the early days of international shipping an is largely unchanged since then.

In the CIP rule, the goods are transferred when they are delivered to the first carrier, while in the CIF rule when the goods are loaded on a mean of transport.

Also, unlike the CFR rule, in the CIP rule, the seller is responsible for concluding the contract and paying the cost of insuring the goods to the buyer.

The difference between CIF and CFR is that while the risk of loss or damage at delivery becomes the buyer’s, the seller is obliged to take out insurance for that risk and provide the buyer with a document which allows the buyer to claim against that insurance. This typically will be an original insurance policy covering just that transaction or a certificate issued by the insurer under the seller’s existing open marine policy. Both of these will normally show the seller as the “insured” or “assured” and will require the seller to endorse the document on the reverse such that the buyer or any bona fides holder with an insurable interest in the goods at the time of loss or damage occurred can claim.

The CIP Incoterms rule imposes on the seller the obligation to conclude a contract of insurance covering the risk of loss or damage to the goods by the buyer from the delivery point to at least the place of destination. This can cause difficulties when the destination country requires purchasing insurance cover on the spot. In this case, the parties should consider selling and buying under the CPT Incoterms rule.

The Incoterms 2010 and Incoterms 2020 revisions differ in the minimum level of insurance cover that must be provided

Only two Incoterms rules (CIF, CIP) refer to freight insurance, which is to be arranged and paid for by the seller.

For the other rules, each party makes a commercial decision as to whether to insure for the part of the journey where they are “on risk”

Incoterms 2010

The level of cover mandated by the CIP and CIF rules is minimal, and may not satisfy the buyer’s requirements. It is Clauses “C” of Institute Cargo Clauses – excludes many risks which many buyers want covered.

Incoterms 2020

The level of cover mandated by the CIF rule is minimal – Institute Cargo Clauses (C). However for the CIP rule, there is a higher level of cover – Institute Cargo Clauses (A).

The rationale is that in general, manufactured goods will require a higher level of insurance cover than commodities.

In all cases, the parties may choose to specify a different level of insurance cover within their commercial agreement.

All freight insurance usually excludes consequential loss, e.g. the knock-on effects of buyer missing a contract deadline or a sales season. This risk can sometimes be included by agreement with the insurer. So the risks to be covered should be discussed and then incorporated into the commercial agreement.

Other considerations for CIP and CIF

- Once the goods have been taken in charge by the carrier (or loaded on board the ship), the buyer is “on risk”, and so must deal with the insurance company in order to make a claim. This has implications for the insurance document that the seller provides – it may need to be appropriately endorsed.

- Some sellers have global freight insurance policies covering all their consignments. This often creates problems for the use of e.g. CIP . (For a single consignment, how can the insurance be costed, and how can arrangements be made allowing a buyer to make a claim?)

- Some sellers find the requirement for the buyer to claim under the insurance policy unsatisfactory from a customer service perspective. In such cases, the seller may agree to take care of claims. A letter of subrogation can be supplied (seller takes over right to claim under the policy)

- Even the highest of the Institute Cargo Clauses – Clauses A – excludes risks that the buyer may think are important – for example War and Strikes (for which a standard Institute clause exists)

CIP Tips And Tricks

- Our CPT tips are also helpful for CIP, except for the tip on the buyer arranging insurance – because in CIP, that’s the seller’s job.

- The seller is required only to arrange minimum insurance cover, to the invoice value of the goods. If the buyer does not consider that coverage sufficient, an agreed level of cover can be included elsewhere in the contract of sale.

- Although the seller is responsible for insurance, the risk transfers to the buyer before the main carriage.

- The seller is not obliged to arrange insurance for pre-carriage in the export country or carriage in the import country unless this is specified elsewhere in the sales contract.