The Russia-Ukraine war is the kind of geopolitics-altering event that should shake up trade flows for years to come, promising big repercussions for shipping shares.

A month into the conflict, American Shipper spoke with Randy Giveans, shipping analyst at Jefferies, about how the war is affecting — or not yet affecting — the stocks in different vessel segments.

There have been some big stock moves already, outperforming the broader stock market. But it’s still too early to see the full impact. “Part of the reason is that we’re in a stalemate,” said Giveans. “For questions like ‘What are the new trade routes going to look like?’ and ‘Will reduced flows be offset by ton-miles [longer distances]?’ it’s very hard to tell after just a month.”

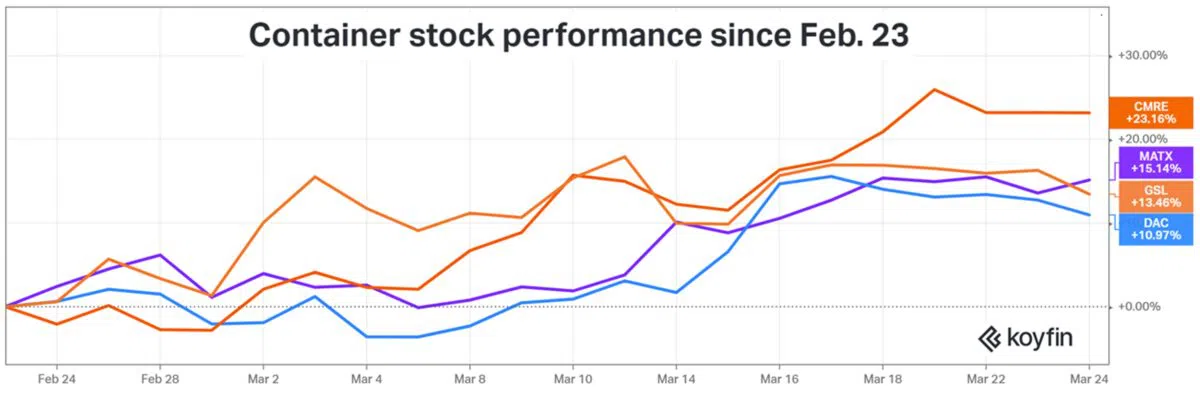

Container shares

Sentiment headwinds are growing for the container sector, both related to the war and unrelated. Inflation accelerated by the war. Potential recession in Europe. Consumer confidence issues in the U.S. The possibility of future sanctions targeting China. A moderate decline in spot rates.

And yet, container shipping stocks continue to strengthen. Container stocks have risen despite the war, not because of it.

According to Giveans, container-ship lessors “just keep signing charters for higher rates, locking in cash flows for three, four, five years. They’re less exposed to near-term headlines.”

Ship lessor Danaos (NYSE: DAC) is up 11% since the start of the war a month ago and 37% year to date (YTD). Costamare (NYSE: CMRE) is up 23% month on month (m/m) and 35% YTD, Global Ship Lease (NYSE: GSL) 13% m/m and 24% YTD.

All charts: Koyfin

Container liner operators are more exposed to indirect fallout from the war, Giveans acknowledged. Even so, Matson (NYSE: MATX) is up 15% since the war began and 34% YTD. Shares of Zim (NYSE: ZIM) — based on adjusted closing prices that account for Tuesday’s dividend — are up 33% m/m and 51% YTD.

In Zim’s case, there have been company-specific drivers moving the stock up. “A lot has happened since the war that is very Zim specific,” said Giveans. “It reported earnings, very strong projections and a dividend that was well above what anyone expected.”

Liner stocks are also being buoyed by investor belief that “port congestion will be persistent,” Giveans added.

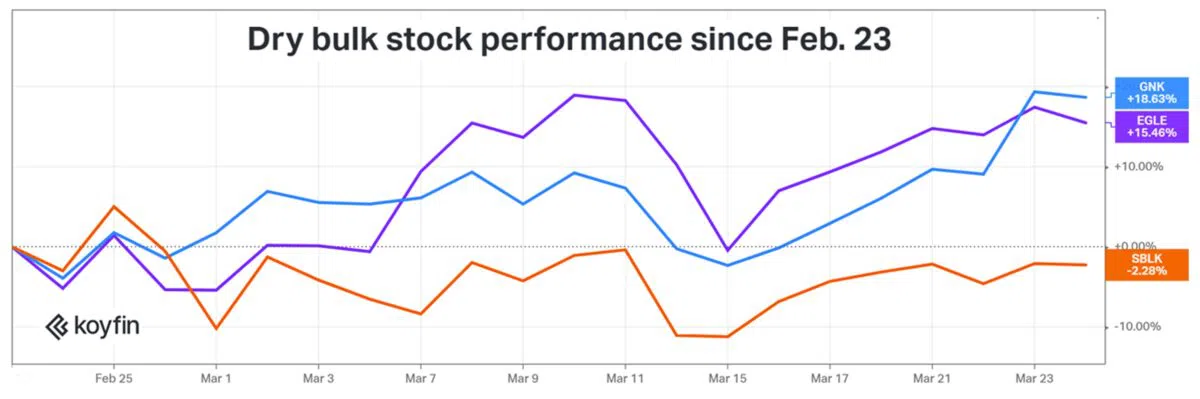

Dry bulk stocks

In the dry bulk sector, the war has the potential to shut in a large volume of agribulk exports from both Ukraine and Russia.

That volume may not be fully replaceable, potentially reducing demand for dry bulk carriers in the Panamax (65,000-99,999 deadweight ton or DTW) and Supramax (50,000-59,999 DWT) categories.

Europe’s need to replace Russian coal with coal from other sources such as Asia is a positive for larger Capesizes (180,000 DWT). But Capes separately face negative pressure from COVID lockdowns in China and losses in the Chinese housing market (Capes carry coal and iron ore used by China to produce steel).

Rates for Panamaxes and Supramaxes are up year on year, whereas Cape rates are down. Amid a mixed bag of indicators, several dry bulk stocks are up double digits.

Genco Shipping & Trading (NYSE: GNK) is up 19% m/m and 45% YTD. Eagle Bulk (NASDAQ: EGLE) is up 15% m/m and 41% YTD. Star Bulk (NASDAQ: SBLK) is down 2% since the start of the war but still up 30% YTD.

“If you look at the dry bulk FFA [freight futures] curve over the last six weeks, it’s only going up for the rest of the year,” said Giveans. “When it comes to Russia-Ukraine, will all of the volume be replaced? I don’t know. But the new trade of coal going from Australia to Europe is extremely long-haul and positive for ton-miles.” (Demand is measured in ton-miles: volume multiplied by distance.)

“The balance sheets of Genco, Star Bulk and Eagle are extremely strong. All three also have extensive scrubber exposure — and not only are day rates great, but scrubber premiums are great too,” said Giveans.

Ships with exhaust-gas scrubbers can burn cheaper 3.5% sulfur fuel as opposed to 0.5% sulfur fuel. The war has pushed up oil prices and widened the spread between the two fuel types, increasing savings for shipowners with scrubbers.

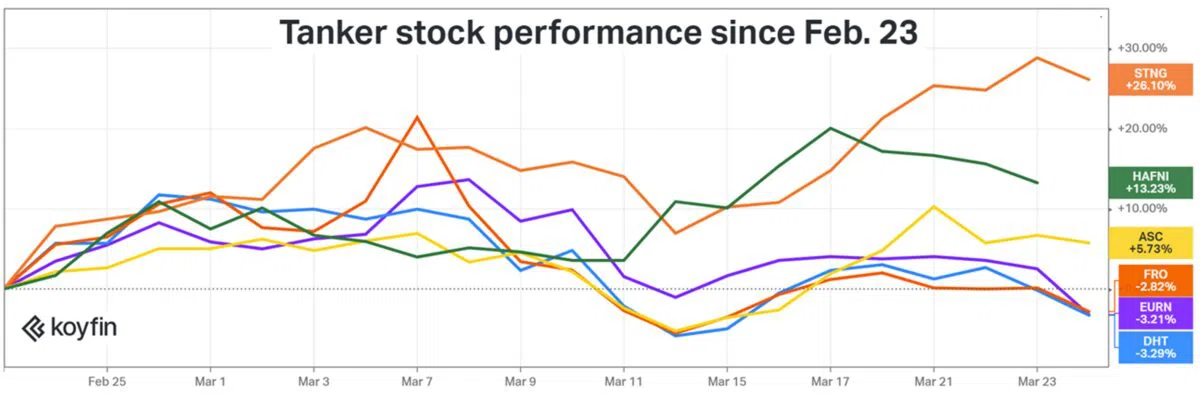

Tanker shares

Tanker stock performance has been mixed over the past month, with several equities jumping initially after the invasion then given back gains.

Listed companies owning very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude) have underperformed.

Euronav (NYSE: EURN) is down 3% since the war began, although still up 13% YTD. DHT (NYSE: DHT) is down 3% m/m and up 5% YTD, with Frontline (NYSE: FRO) down 3% since the war began and up 17% YTD.

“You need to separate crude and products,” said Giveans. “On the crude side there has been no impact yet [from the war]. The rates yesterday [Wednesday] were the worst they’ve ever been for a non-scrubber, non-eco VLCC. There could be some dislocation, with more Russian crude to China and India and Western Europe importing more from the U.S., Latin America and the Middle East. But it will take time. I’m pretty optimistic about 2023, but the next few months could see some headwinds.”

Product tanker stocks have fared much better.

Scorpio Tankers (NYSE: STNG) is up 26% since the war began and 56% YTD. Ardmore Shipping (NYSE: ASC) is up 6% m/m and 31% YTD. Oslo-listed Hafnia is up 13% m/m and 21% YTD.

“On the product side, the effect is more immediate [than for crude],” said Giveans.

“You’re seeing more robust diesel flows to Western Europe [from farther afield, replacing] a lot that had been coming from Russia. Product tankers are certainly benefiting more and are being more positively disrupted than crude tankers, so they should be outperforming crude stocks from an equity perspective over the past month.”

Copyright Freightwaves.com 2022

By Gregg Miller